On the Wikipedia page: "Supply and demand", it states that "Supply and demand is an economic model based on price, utility and quantity in a model. It predicts that in a competitive market, price will function to equalize the quantity demanded by consumers, and the quantity supplied by producers, resulting in an economic equilibrium of price and quantity. The model incorporates other factors changing equilibrium as a shift of demand and/or supply".

On the Wikipedia page: "Supply and demand", it states that "Supply and demand is an economic model based on price, utility and quantity in a model. It predicts that in a competitive market, price will function to equalize the quantity demanded by consumers, and the quantity supplied by producers, resulting in an economic equilibrium of price and quantity. The model incorporates other factors changing equilibrium as a shift of demand and/or supply".Pretty heavy stuff, but the basic stuff is:

If the demand for the product increases, then the manufacturer would increase the price of the product.

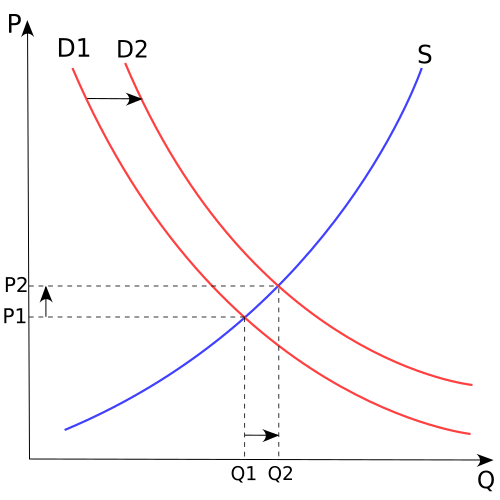

If a new type of game came out, the price would not e decided by the manufacturer, nor the consumer, but the market forces, or the equilibrium point.

The equilibrium point is where the price (p) meets the quantity (q) at the dotted lines.

For example: The price of shoes would go up if the demand for them also went up, but the price wouldn't go up if nobody was buying them.

That's about all I'll write for now, though I haven't covered a lot of it.

0 comments:

Post a Comment